Insights

Natural Catastrophe Sublimits: Determining How Much Insurance To Buy In A Turbulent Insurance And Project Finance Environment

Jul 18, 2023

Recent renewable energy project finance transactions have highlighted the potential discrepancy between what renewable energy project stakeholders would like in an insurance program and what the insurance market is willing to provide. Nowhere is this more apparent than in the negotiation surrounding the appropriate amount of coverage for natural catastrophe (Nat Cat) perils.

Traditional all-risk property policies for renewable energy projects cover all perils for their total insurable value, except where specifically excluded or with reduced limits, i.e., “sublimits.” Sublimits have historically been imposed on the Nat Cat perils of earthquakes, hurricanes, and floods. More recently, sublimits have also been imposed on severe convective storms (including hail and tornadoes) and wildfires.

For example, for a $100M solar project in California, $100M in earthquake coverage would be cost-prohibitive and has not traditionally been contractually required by financing parties. Instead, a sublimit that reflects all parties’ comfort levels around the likelihood of an earthquake during the policy term is agreed upon and procured. The same logic is applied to all Nat Cat perils, including floods, hurricanes, hail, and wildfires.

There is no real consensus on the “right” way to establish an appropriate sublimit, which creates a great deal of uncertainty for project developers.

WHY DOES IT MATTER

The sublimit is a key element of the insurance program for a project or portfolio of assets that a financing party will require in order to proceed with financing, and it is often a main driver of the overall insurance cost. For example, if you have a hail-exposed solar project, the premium difference between $20M in hail coverage versus $50M in hail coverage could be enough to cause the project to no longer pencil. Therefore, it is imperative that this figure be matched to the risk tolerance of the parties and reflect the likelihood of a loss.

HOW HAS THIS BEEN HANDLED TO DATE?

Nat Cat statistical modeling software is generally used to provide a snapshot of the exposure associated with the various Nat Cat perils for a project or portfolio. Modeling results provide probable maximum loss (PML) estimates for a range of return intervals, which are useful in understanding the magnitude of anticipated damage should a Nat Cat event occur. There are a handful of models commonly used throughout the industry. Many insurers also rely on this modeling when underwriting a project or portfolio of assets.

For assets in high-hazard zones for Nat Cat perils, financing parties historically required the asset owner to procure a sublimit not less than 125% of the 1-in-500-year PML for each peril. However, it is common for financing parties to require higher limits in the case of large loan values or credit committee standards. For assets in low-hazard zones, financing parties will typically require no less than 25% of TIV if full limits are not available. This rule of thumb was considered “industry standard” and was generally consistent for the past 15 years of renewable energy project development, which allowed project owners and developers to obtain reliable estimates for insurance costs that accounted for anticipated requirements.

WHAT HAS CHANGED

A variety of factors have converged to create a moment in which there is no real consensus on the “right” way to establish an appropriate sublimit, which creates a great deal of uncertainty for project developers. These factors include large losses that in some cases have exceeded the sublimit on the policy and reduced confidence in whether the models are able to accurately estimate PMLs for renewable energy technology. In addition, models are not able to factor in the resilience or mitigating features of a project. These features may lead to different outcomes that could be uniformly addressed throughout the industry.

Naturally, the limits procured for Nat Cat perils for a project are a significant driver in its insurance costs. Without certainty at the outset of project development on what level of coverage will be required, it has become increasingly difficult to include meaningful estimates of insurance costs in financial models. Since requirements are generally not known until a project is being financed, there is limited ability for the owner or developer to adapt to these new realities. This has created many challenging discussions at the intersection of finance and insurance, even delaying closings.

WHAT IS THE CURRENT STATE OF PLAY?

Projects are getting larger, deploying new technologies, and moving into more marginal locations from a Nat Cat standpoint. At the same time, insurers are continuing to pay out claims for sizable Nat Cat and equipment failure losses. This has created a moment where Nat Cat capacity is limited, expensive, and more in demand than ever before.

Many financing parties are adopting their own determinations of appropriate sublimits that match their specific risk tolerances, and the previous “industry standard” approach no longer applies. There is a two-fold effort underway to improve the working understanding of the actual modeled risk.

- A great deal of work is going into creating models that match specific perils with the equipment that is exposed. For example, VDE Americas is creating a model that can account for specific equipment and design choices in determining PMLs for hail. Such models can give great insight into the value of specific resilience measures in improving the overall risk profile of a site.

- Engineered PMLs are becoming increasingly common in negotiating appropriate sublimits. In these cases, a combination of qualitative and quantitative approaches are used to determine a PML, and specific attributes of a system that cannot be picked up by modeling software are incorporated into the analysis.

Without certainty at the outset of project development on what level of coverage will be required, it has become increasingly difficult to include meaningful estimates of insurance costs in financial models.

WHAT CAN BE DONE TO NAVIGATE THIS NEW REALITY?

Project owners and developers must fully comprehend the exposures at their project site(s), the value of resilience investments in fortifying the infrastructure for specific weather regimes, and their partner’s risk tolerance for physical damage. The earlier such knowledge is available, the better.

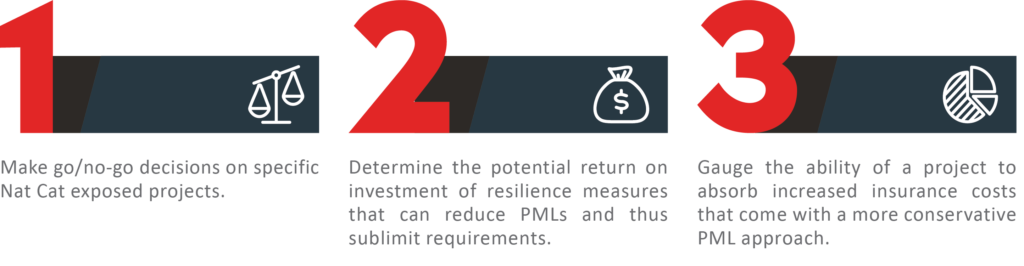

Projects can use this information in a variety of ways, including but not limited to:

CAC Specialty and Cirrus Advisers help our clients navigate this new terrain every day. We help our clients assess their risk, source the reports that will assist in important decision-making around Nat Cat resilience measures and represent these enhancements to both financing parties and underwriters. Much of this work happens well in advance of the need to purchase insurance. This is a fast-evolving space, and it is crucial that project owners and developers choose brokers and partners that understand the nuances of this market. We encourage you to contact us to learn more about how we can assist.

WHAT’S UP NEXT?

In the final installment, we will suggest our views on how to streamline the process to financial close with respect to insurance considerations, which are playing an increasingly important role in the path to financing.

CAC Specialty’s Power and Renewables Team Is Here To Assist

As a specialty property and casualty insurance brokerage firm, we spend our days speaking with owners and operators of renewable energy assets about what they can expect out of the insurance market in terms of coverage and cost during both construction and operations. Our role is to find the most competitive insurance program for these assets that balances breadth of coverage with expense. We are a team of professionals that includes former risk managers from both renewable energy and traditional power companies, a former lenders’ advisor at one of the preeminent lenders’ advisory firms, loss control engineers, investment professionals and some of the most tenacious, dedicated insurance brokers in the business, who have spent their careers successfully navigating the insurance market for all types of power generating assets. In many cases, we act as outsourced risk managers to our clients who do not have dedicated insurance professionals on their teams, and we pride ourselves on our hands-on approach to helping our clients in all aspects of the insurance transaction, especially as it intersects with their project finance efforts.

We help our clients determine appropriate coverages, place those coverages in a constantly evolving insurance marketplace, and negotiate insurance concerns with their stakeholders. In parallel, we look to educate insurers about evolving areas of risk that our clients are facing and develop new tools to give the industry a clearer view of risk. Our work puts us across the table from underwriters with the goal of obtaining the best possible policy coverage, terms, and conditions for our clients’ current and future projects. We also interact with financiers, typically via their insurance advisors, where we work on behalf of our clients to negotiate reasonable and customary insurance requirements for non-recourse project financings.

SARA KANE

Power & Renewables Practice Leader

sara.kane@cacspecialty.com