Insights

Energy Challenges: Battery Energy Storage

Apr 5, 2023

Renewable Energy Project Risk & Insurability in a Turbulent Insurance Market

One of the most exciting technological developments of recent years is the rapid expansion and use of battery energy storage systems (BESS) to enhance traditional power generation and renewable energy projects while providing grid stability. The global battery energy storage market is projected to grow from $10.88 billion in 2022 to $31.20 billion by 2029, at a CAGR of 16.3% in forecast period.

However, this growth is likely to be tempered by the insurance community’s perceptions regarding the safety of these installations. The task for underwriters is made considerably more challenging by the rapid rate of technological change and underwriters’ struggle to keep pace. In this piece we will look at 1) a brief overview of the technical challenge at hand, 2) the limited history of battery energy storage systems in the insurance market, 3) how the insurance view can impact the scaling of the technology, and 4) what brokers, sponsors, OEMs, insurers and the financing community can do.

A Brief History of Bess within Insurance Markets

The use of batteries in large scale energy applications dates back to 2008, when the first BESS was connected to the grid. Since that time, the industry has undergone remarkable technological change, all in the pursuit of increased safety and efficiency. Early systems used Nickel-Manganese-Cobalt (NMC) chemistry, the same batteries being used by electric vehicles. These batteries were advantaged by high energy density and high maximum charge voltages. Their disadvantages include limited life cycles and potential fire risk from thermal runaway events. There has been a move by industry to lithium iron phosphate (LFP) batteries over the last 5 years. The loss of energy density of these systems is offset by the benefits of improved lifecycles. Importantly, the fire safety of this chemistry is also considered superior as LFP batteries are less likely to initiate a fire during a thermal runaway event and must reach significantly higher temperatures to go into thermal runaway.

One significant improvement in the last few years has been the increased implementation of and continued enhancements to battery management systems (BMS); systems that monitor, control, and optimize the performance of battery modules. Battery management systems now have an improved ability to identify issues within the individual battery cells and automatically shut down and isolate batteries prior to failure. In addition, many companies are now offering analytic programs that take information from the BMS and use that data to monitor and predict many BESS issues including imminent cell failure, thus eliminating many, if not all, progressive BESS failure events before they happen.

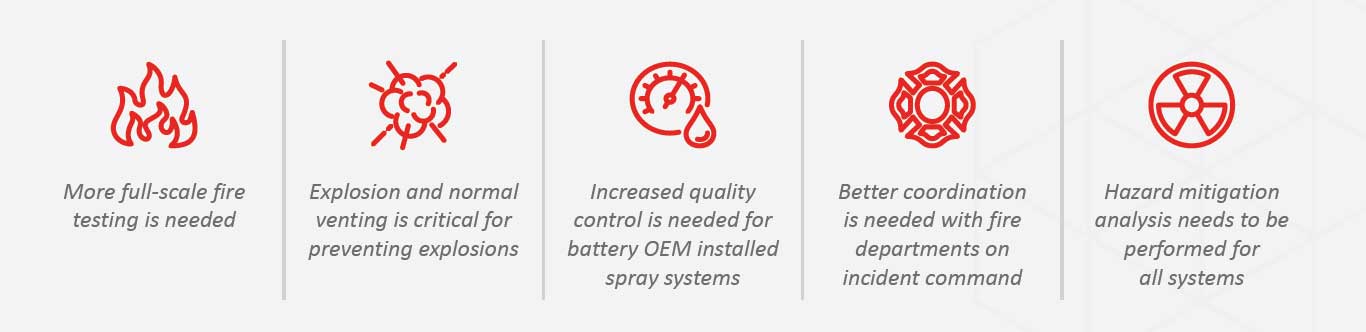

While industry continues to pursue improvements to storage technologies, insurers have grappled with a few large losses. In 2012, the first of these large losses caused insurers to adopt a much more cautious position as they beefed up their engineering capabilities to keep up with technological advancements. The Electric Power Research Institute (EPRI) maintains a database tracking reported energy storage system fires. Currently, the database has 47 events for gridscale type applications, recording events from 2011 onward. This is probably not a complete data set, but it is the most comprehensive currently available.

How do Insurers Impact Scaling?

The conservative approach of insurers can impact the scaling of new storage technologies in many ways. Most significantly, the inability of a sponsor to procure sufficient insurance coverage to match a bank’s risk tolerance can prevent a project from being financed. This is amplified as the appetite of insurers changes as the loss history evolves, which could leave projects that use a technology “stranded” if such losses develop between project development and financing. For example, our team recently went to market for such a project and canvassed the entire insurance market for a solution. The effort involved significant time and energy from the broker and sponsor over a three-month period, including submissions to 54 markets and a dozen market engineering focused calls with multiple insurers on each call.

The result was six quotes of which two were non-viable due to unreasonable terms. The remaining four insurers provided workable quotes as they were able to commit the time and energy necessary to the project. The final result exceeded expectations but required meaningful investment of time and expertise. The experience was indicative of the real challenge that persists for new, misperceived, misunderstood or difficult exposures.

Ultimately, if a project is not insurable, it is not financeable. We are not currently aware of any such projects, but the pace of advancements in battery energy storage technology and the concurrent evolution of insurer appetite warrants a close watch and understanding of these dynamics.

Lessons Learned from the EPRI Data Set Would Suggest the Below:

These 47 events took place at projects that totaled approximately 4.1GWh. For reference, at the end of 2021, it is estimated that there were 27GW/56GWh installed globally. It is estimated that another 387GW/1,143GWh will be added globally between 2022 and 2030.

Regardless, while the number of events is small relative to the deployment of the technologies worldwide, the magnitude of the losses combined with the pace of continued change makes insuring these systems a challenge. For example, one of these losses is estimated to have cost insurers more than $100M.

How can the Insurance Community Spur Innovation?

There is a great history of the insurance market responding to technological change in a way that promotes safety, efficiency and commitment to innovation. For example, the safety mechanisms present in our daily lives of airbags4 and sprinkler systems5 are due in large part to advocacy from the insurance community. Our team has no doubt that the insurance community will meet this challenge in the same way. However, this evolution takes time, and we are just putting these projects in the ground today. What does that mean for the role each of us plays in promoting this transition?

Sources: 4. https://www.iihs.org/media/186adabe-9ef4-479c-ad37-36b9f0e7fca1/Ka0wWQ/Albaum_Safety_Sells.pdf 5. https://nfsa.org/aboutnfsa/

De-Risking Bess for the Green Energy Transition

The rapid expansion of battery energy storage systems (BESS) within the last decade presents a unique challenge to the modern insurance community. Battery energy storage systems have the potential to bolster the green energy transition by enhancing the efficiency of renewable energy sources, reducing the need for traditional fossil fuel-based power plants and improving overall grid resiliency, which can materially reduce energy costs.

Despite their promise, insurers remain wary of BESS due to their limited history, misperceived risk profile and first-generation loss events. Early systems used batteries prone to thermal runaway events and lacked the sophisticated management technology of today, which has greatly reduced the likelihood of BESS failure events. Lingering reputational damage, combined with significant capital expenses needed for installation, maintenance and specialized expertise, has stymied the widespread scaling of BESS.

Brokers, insurers, sponsors, underwriters and financiers can collectively work to de-risk this innovative technology by advocating for the continued education of the insurance and regulatory communities, providing coverage on a case-by-case basis, rather than wholly eliminating subcategories of industry, improving data sets and loss history for the technology, and providing insurance solutions for emerging BESS safety enhancements. Only by delivering greater clarity and certainty for both insurers and clients can we hope to meet or surpass the ambitious energy installation targets of 2030.

What’s Up Next?

In the third installment, we will spend time on a second pervasive issue – determining the appropriate amount of natural catastrophe coverage considered adequate by all project stakeholders, without being cost-prohibitive to the project. In this post, we will describe the current methods and offer some alternatives.

In the final installment, we will suggest our views on how to streamline the process to financial close with respect to insurance considerations, which are playing an increasingly important role in the path to financing.

CAC Specialty’s Power and Renewables Team Is Here To Assist

As a specialty property and casualty insurance brokerage firm, we spend our days speaking with owners and operators of renewable energy assets about what they can expect out of the insurance market, in terms of coverage and cost during both construction and operations. Our role is to find the most competitive insurance program for these assets that balances breadth of coverage with expense. We are a team of professionals that includes former risk managers from both renewable energy and traditional power companies, a former lenders’ advisor at one of the preeminent lenders’ advisory firms, loss control engineers, investment professionals and some of the most tenacious, dedicated insurance brokers in the business, who have spent their careers successfully navigating the insurance market for all types of power generating assets. In many cases, we act as outsourced risk managers to our clients who do not have dedicated insurance professionals on their teams, and we pride ourselves on our hands-on approach to helping our clients in all aspects of the insurance transaction, especially as it intersects with their project finance efforts.

We help our clients determine appropriate coverages, place those coverages in a constantly evolving insurance marketplace, and negotiate insurance concerns with their stakeholders. In parallel, we look to educate insurers about evolving areas of risk that our clients are facing and develop new tools to give the industry a clearer view of risk. Our work puts us across the table from underwriters with the goal of obtaining the best possible policy coverage, terms, and conditions for our clients’ current and future projects. We also interact with financiers, typically via their insurance advisors, where we work on behalf of our clients to negotiate reasonable and customary insurance requirements for non-recourse project financings.